Navigating the complexities of health insurance can be daunting, particularly with high deductible health plans (HDHPs) gaining popularity. This article delves into the intricacies of HDHPs, offering expert perspectives, practical insights, and real examples to guide informed decisions.

Understanding High Deductible Health Plans

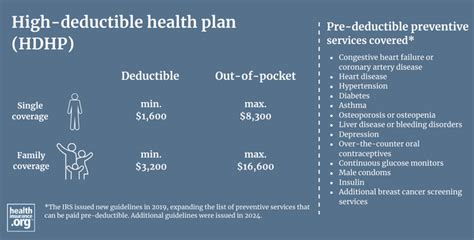

High deductible health plans have become a cornerstone of health insurance reform, striking a balance between cost-sharing and comprehensive coverage. An HDHP typically has a lower monthly premium but a significantly higher deductible. To qualify for an HDHP, the deductible must generally exceed 1,400 for an individual or 2,800 for a family. Coupled with these high deductibles, HDHPs offer tax-advantaged Health Savings Accounts (HSAs). These accounts allow individuals to save pre-tax dollars for qualified medical expenses, providing an additional financial cushion.

Strategic Financial Planning for HDHPs

With the rising prevalence of HDHPs, strategic financial planning is essential. Individuals need to assess their health care costs and determine if they can meet the high deductible threshold. A practical approach involves evaluating past medical expenses, anticipated future costs, and the potential savings from lower premiums. For instance, a family with minimal health issues might find an HDHP more advantageous due to the substantial savings on premiums. However, families with chronic health conditions must weigh the deductible against their expected medical expenditures. One technical consideration involves understanding the out-of-pocket maximum, which caps the total annual out-of-pocket costs, offering a safeguard against excessive healthcare expenses.

Key Insights

Key Insights

- HDHPs balance lower premiums and higher deductibles, ideal for individuals with predictable health care needs.

- Understanding the out-of-pocket maximum is crucial in assessing the true cost of an HDHP.

- Utilize Health Savings Accounts (HSAs) to maximize the tax benefits and financial flexibility offered by HDHPs.

Navigating the Benefits of HSAs

One of the most compelling aspects of HDHPs is the availability of Health Savings Accounts (HSAs). HSAs are unique in their tax advantages, allowing funds to grow tax-free, be invested, and used for qualified medical expenses without penalty. For instance, an individual can use HSA funds for deductibles, copayments, prescriptions, and even long-term care services. This can be especially beneficial during retirement when healthcare costs typically increase. However, it’s important to adhere to the rules regarding HSAs; funds used for non-qualified expenses result in taxes and penalties, similar to an IRA distribution.

Maximizing the Potential of HDHPs

To maximize the potential of HDHPs, individuals should implement a multi-faceted strategy. First, consider the full spectrum of available medical services. Using preventive care services can reduce overall healthcare costs, as many HDHPs cover preventive care like screenings and vaccines without a deductible. Additionally, establishing an emergency fund is prudent, providing a safety net for unexpected medical expenses. Lastly, regular consultations with a financial advisor can help tailor a health insurance plan that aligns with personal health and financial goals.

FAQ Section

Can I use HSA funds for non-medical expenses?

No, funds used for non-qualified medical expenses result in taxes and penalties, akin to an IRA distribution. It’s crucial to adhere to the IRS guidelines to avoid these penalties.

Is it worth keeping the HDHP if I’ve had significant health issues in the past?

Deciding whether to keep an HDHP with significant past health issues requires a detailed evaluation. Consider the cost of the high deductible versus the benefits of lower premiums. Additionally, review potential out-of-pocket costs and explore options for supplemental insurance that may provide necessary coverage without exceeding budget constraints.

In summary, while high deductible health plans require careful financial planning and consideration, they offer significant benefits, particularly through Health Savings Accounts. By strategically managing medical expenses and leveraging HSA funds, individuals can optimize their healthcare financial strategy.