Understanding High Deductible Health Plans vs. PPOs: A Comprehensive Guide

Navigating the landscape of health insurance can be overwhelming. Two prominent types of health plans often come up in discussions: High Deductible Health Plans (HDHPs) and Preferred Provider Organizations (PPOs). Both have their unique advantages and potential pitfalls. This guide will provide you with a step-by-step understanding, practical solutions, and actionable advice to help you choose the best health plan for your needs.

The Challenge: Choosing the Right Health Plan

Choosing between a High Deductible Health Plan and a PPO can be a daunting task. Each plan has its benefits and drawbacks. HDHPs often come with lower monthly premiums but higher out-of-pocket costs when you need significant medical care. On the other hand, PPOs typically have higher monthly premiums but lower out-of-pocket costs for more extensive medical care. Understanding these differences and how they impact your healthcare decisions is crucial for making an informed choice.

This guide will help you decipher these complex options with practical, real-world examples and solutions tailored to address your specific healthcare needs and financial situation.

Quick Reference

Quick Reference

- Immediate action item: Compare your annual medical costs with premiums and deductibles.

- Essential tip: For routine care, lower monthly premiums might be beneficial. For unpredictable high costs, consider out-of-pocket expenses.

- Common mistake to avoid: Assuming HDHPs are cheaper overall without considering long-term healthcare needs.

High Deductible Health Plans (HDHPs): How They Work

High Deductible Health Plans are characterized by their significantly higher deductibles compared to standard health plans. Here’s a deeper dive into how they function and how to best navigate them.

Understanding the structure of HDHPs can help you leverage their benefits while managing potential downsides effectively.

Detailed How-To: Navigating HDHPs

An HDHP is typically paired with a Health Savings Account (HSA). Here’s how you can maximize the benefits of this setup:

Understanding HDHPs

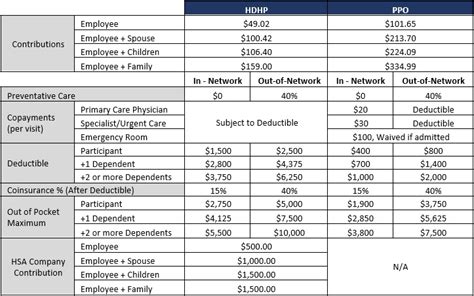

HDHPs are defined by annual deductibles of at least 1,400 for individual coverage and 2,800 for family coverage in 2022. The out-of-pocket maximum is capped at 7,050 for individual coverage and 14,100 for family coverage. The key advantage of an HDHP is the lower monthly premium.

Here's a step-by-step guide to understanding and leveraging your HDHP:

Step 1: Calculate Your Expected Medical Expenses

Before enrolling in an HDHP, estimate your medical expenses for the year. This includes routine check-ups, prescriptions, and any anticipated major medical procedures. Comparing these costs with your HDHP’s deductible will give you a clearer picture of potential savings.

Step 2: Set Up a Health Savings Account (HSA)

Since HDHPs are paired with HSAs, setting up an HSA is crucial. HSAs allow you to save pre-tax dollars for qualified medical expenses. Contributions can be made by you, your employer, or both. The money in an HSA grows tax-free, and withdrawals for qualified medical expenses are also tax-free.

Step 3: Maximize HSA Contributions

To get the most out of your HDHP, max out your HSA contributions each year. In 2022, the HSA contribution limit is 3,650 for individual coverage and 7,300 for family coverage, with an additional $1,000 catch-up contribution allowed for those aged 55 and older. This can provide a significant financial cushion for unexpected medical expenses.

Step 4: Manage Out-of-Pocket Costs

Since HDHPs come with high deductibles, it’s important to have a strategy for managing out-of-pocket costs. This could involve setting aside an emergency fund or considering flexible spending accounts (FSAs) for eligible medical expenses. Keeping a separate savings account for medical expenses can help bridge the gap during the deductible period.

Step 5: Utilize Preventive Services

HDHPs often cover preventive services like vaccinations, screenings, and wellness visits at no cost. Take advantage of these services to maintain your health and avoid larger medical bills later. Most HDHPs offer these services without any out-of-pocket costs.

Preferred Provider Organizations (PPOs): Understanding Their Structure

PPOs provide a network of doctors and hospitals with whom they have contracts. The advantage of a PPO is greater flexibility in choosing healthcare providers without needing referrals. Here’s how to make the most of a PPO plan.

Detailed How-To: Navigating PPOs

PPOs are flexible and offer extensive network options, but they come with their own set of rules and potential drawbacks. Here’s how to navigate them effectively:

Step 1: Understand Network vs. Out-of-Network Care

PPOs provide coverage for both in-network and out-of-network care, though out-of-network services typically come with higher costs. Familiarize yourself with your plan’s network to make informed decisions about your healthcare providers.

Step 2: Manage Out-of-Pocket Costs

PPOs have copayments, coinsurance, and deductibles. Knowing these costs in advance helps you plan your healthcare expenses better. For minor procedures or routine care, in-network providers usually offer lower out-of-pocket costs.

Step 3: Choose Your Primary Care Physician (PCP)

PPOs often require selecting a PCP, who will coordinate your care and provide referrals to specialists. Choose a PCP who is within the network and convenient for you. This can help streamline your care and potentially reduce your costs.

Step 4: Understand Referral Requirements

While PPOs generally don’t require referrals to see specialists, understanding any referral policies within your specific plan is crucial. This helps avoid unexpected out-of-pocket costs and ensures you’re getting the most out of your plan.

Step 5: Review Your Benefits Regularly

PPOs often have benefits that can change annually. Reviewing your benefits regularly helps you stay informed about any changes and enables you to make the best healthcare decisions for your needs.

FAQ Section

Can I use an HDHP with an HSA indefinitely?

Yes, you can use an HDHP with an HSA indefinitely as long as you meet the eligibility criteria. The money in your HSA rolls over year to year, and you can use it to cover qualified medical expenses at any time. However, if you switch to a plan that isn’t an HDHP, you can no longer contribute to your HSA, but you can still use the funds for qualified medical expenses.

Are preventive services free under an HDHP?

Yes, HDHPs generally cover preventive services at no cost. This includes routine check-ups, screenings, and vaccinations without any out-of-pocket costs. Taking advantage of these services can help you avoid larger medical bills in the future.

Why might I choose a PPO over an HDHP?

You might choose a PPO if you prefer flexibility in choosing healthcare providers without the high deductibles of an HDHP. PPOs generally have lower out-of-pocket costs for in-network care and provide more extensive networks. This can be beneficial if you anticipate needing frequent medical care or specialist visits.

Conclusion

Choosing between a High Deductible Health Plan and a PPO requires a careful evaluation of your healthcare needs and financial situation. By understanding the intricacies of each plan, leveraging the benefits