Navigating the complexities of healthcare finance involves understanding tools like Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs). While both these accounts are designed to help individuals manage out-of-pocket medical expenses, they have distinct features, benefits, and drawbacks. This article provides a focused professional perspective to distinguish between HSAs and FSAs, offering evidence-based insights and practical examples to aid informed decision-making.

Whether you're a financial planner or a healthcare consumer, comprehending the intricacies of HSAs and FSAs is crucial for optimizing medical expense management. An HSA, as an out-of-pocket healthcare financing tool, comes with a trifecta of benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. In contrast, FSAs provide pre-tax spending options for medical expenses but often have a use-it-or-lose-it policy. Despite these differences, both accounts aim to alleviate the financial burden of healthcare costs. Let's delve deeper into these distinctions.

Key Insights

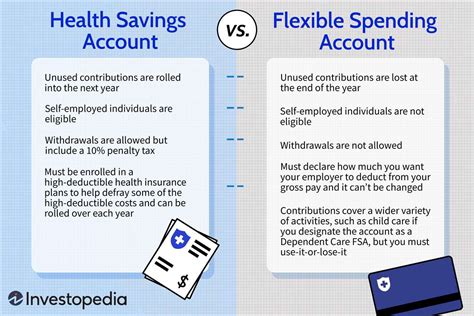

- HSAs offer tax advantages, including tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

- FSAs provide pre-tax medical expense reimbursement but typically have a use-it-or-lose-it policy for unused funds.

- Choosing between HSAs and FSAs depends on your healthcare needs, employer offerings, and personal financial situation.

Health Savings Accounts (HSAs): Comprehensive Benefits

Health Savings Accounts are unique in their combination of tax advantages and the ability to roll over unused funds year to year, with the option to invest for potentially higher returns. Contributions to an HSA are tax-deductible, the funds grow tax-free, and qualified withdrawals for medical expenses are also tax-free. This triple tax advantage can be a substantial benefit, particularly for those expecting high medical costs in the future. For instance, consider a family with an HSA contributing to their retirement healthcare savings, allowing for tax-free accumulation and withdrawal of funds for medical expenses across decades.

Flexible Spending Accounts (FSAs): Immediate Spending Benefits

Flexible Spending Accounts are designed for immediate medical expense reimbursements and offer immediate tax benefits by allowing employees to use pre-tax dollars to cover eligible expenses, such as co-payments, prescription drugs, and sometimes dependent care costs. However, one significant limitation is the “use-it-or-lose-it” policy. Unlike HSAs, FSAs do not roll over unused funds; what is not spent by the end of the plan year is forfeited. For example, a professional with an FSA might choose to spend their allocation on immediate healthcare costs to avoid losing any unspent funds, balancing between immediate needs and potential loss.

Which account is better for someone with high and unpredictable medical expenses?

An HSA might be more advantageous due to its ability to roll over unused funds and invest them for growth, providing a hedge against future unpredictable medical costs.

Can HSA funds be used for non-medical expenses?

Only qualified medical expenses can be reimbursed tax-free from an HSA. Non-medical use of HSA funds results in taxes and potentially a penalty unless the account holder is over age 65 or meets other specific IRS conditions.

In conclusion, the decision between HSAs and FSAs hinges on individual circumstances, including healthcare needs, employer benefits, and financial goals. HSAs provide a powerful trifecta of tax advantages and the ability to save for long-term medical expenses and retirement, while FSAs offer immediate tax benefits for medical expenses without the rollover feature. Understanding these nuances enables more informed choices, ensuring optimal healthcare financial management.