Navigating the world of healthcare savings can feel daunting, but breaking it down into digestible parts can make it manageable. Understanding the differences between a Health Savings Account (HSA) and a Flexible Spending Account (FSA) is crucial to optimizing your healthcare expenses. This guide will demystify these financial tools, providing actionable advice to help you make the best choice for your needs.

Understanding Your Health Savings Options

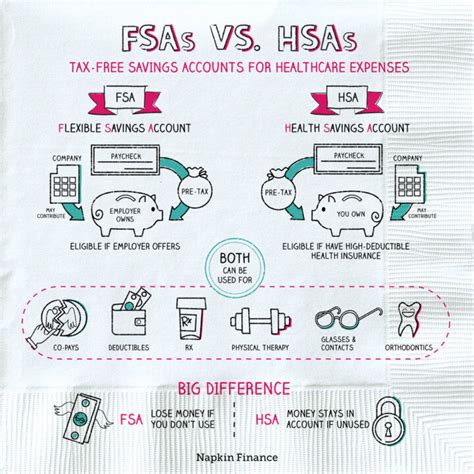

Both Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) allow you to pay for qualified medical expenses using pre-tax dollars. However, they function differently, and each has distinct advantages and drawbacks. The key is to assess your healthcare spending habits and future healthcare needs to determine which option suits you best.

If you're considering an HSA or an FSA, it's important to know what each entails, including how contributions are made, how funds can be used, and what happens if you don’t spend your balances by the end of the year. Let's dive into a quick reference to highlight these points.

Quick Reference

- Immediate action item with clear benefit: Check if you are enrolled in a high-deductible health plan (HDHP) as you must have this to contribute to an HSA.

- Essential tip with step-by-step guidance: For an HSA, maximize contributions annually to take full advantage of tax-deferred growth and tax-free withdrawals for qualified medical expenses. For an FSA, choose your contribution carefully based on your projected healthcare costs for the year.

- Common mistake to avoid with solution: One common mistake is leaving unused FSA funds at the end of the year. To avoid this, either spend the funds wisely throughout the year or transition to an HSA if possible, since HSAs roll over year to year.

Health Savings Account (HSA)

An HSA is a tax-advantaged account specifically designed to help individuals save for medical expenses, and it can be particularly beneficial if you are enrolled in a high-deductible health plan (HDHP). Contributions are made pre-tax, grow tax-free, and can be withdrawn tax-free for qualified medical expenses.

Here’s how to get started with an HSA:

Step-by-step Guidance on Opening an HSA

To open an HSA, you need to meet specific eligibility criteria:

- You must have a high-deductible health plan (HDHP) and no other health coverage.

- You cannot be enrolled in Medicare.

- You cannot be claimed as a dependent on someone else's tax return.

Once you’ve confirmed your eligibility, follow these steps:

- Choose an HSA Provider: Select a bank or financial institution that offers HSA accounts. Popular choices include Fidelity, Vanguard, and HealthEquity. Each provider may have different fees, so it’s important to compare them.

- Complete the Application: Fill out the application form provided by your chosen HSA provider. This will typically include personal information and details about your HDHP.

- Fund Your HSA: You can contribute to your HSA via your employer, yourself, or family members. Contributions can be made via direct deposit, check, or electronic transfer. The maximum annual contribution limit for 2023 is $3,850 for individuals and $7,750 for families.

- Use Your HSA: You can use your HSA to pay for qualified medical expenses, including copayments, deductibles, prescriptions, and more. Remember, the funds can also be invested, potentially growing over time.

It’s important to keep track of your withdrawals and ensure they are for qualified medical expenses. You can use the IRS’s HSA model plan for reference, which lists what expenses are qualified.

An HSA is a powerful tool for long-term healthcare savings, particularly if you have a HDHP. The funds roll over year to year, and once you turn 65, you can use your HSA for any expense, not just medical ones, though it will be taxed if used for non-qualified expenses.

Flexible Spending Account (FSA)

An FSA allows you to set aside pre-tax dollars to pay for eligible medical expenses. There are two types of FSAs: health care FSAs and dependent care FSAs. While both provide tax benefits, they have different purposes and rules.

Here’s how to navigate an FSA:

Step-by-Step Guidance for Setting Up and Using an FSA

To participate in an FSA, follow these steps:

- Review Eligibility: Your employer must offer an FSA, and you must be enrolled in the plan. FSAs are often available through benefits packages at work.

- Choose Your Contribution: Decide how much you want to contribute to your FSA. Contributions are made on a pre-tax basis, reducing your taxable income. For 2023, the limit is $2,650.

- Complete the Enrollment Form: Fill out the enrollment form provided by your employer. This form typically includes your chosen contribution amount and personal details.

- Use Your FSA: Pay for eligible expenses such as co-pays, prescriptions, and some over-the-counter medications. Some FSAs offer a grace period or allow carryover of a small amount, but most FSAs have a use-it-or-lose-it rule.

One of the main drawbacks of an FSA is that any unused funds typically expire at the end of the year or the plan’s grace period (if applicable). However, if your FSA allows for a carryover, it can be a valuable tool for managing predictable healthcare costs.

Tips and Best Practices

Here are some actionable tips to maximize your FSA:

- Predict your medical expenses carefully when choosing your contribution amount to avoid wasting funds.

- Use receipts to keep track of expenses and ensure they are eligible for reimbursement.

- For dependent care FSAs, coordinate with your spouse if both of you have FSAs to optimize your contributions.

Practical FAQ

Can I use my HSA or FSA for non-medical expenses?

No, both HSAs and FSAs can only be used for qualified medical expenses as defined by the IRS. For HSAs, if you use your funds for non-qualified expenses before age 65, you’ll pay a penalty tax. FSAs generally also have penalties and taxes for non-qualified expenses.

What happens to my HSA or FSA if I leave my job?

If you leave your job, you have options for your HSA or FSA:

- Keep your HSA even if you leave your job; you can continue to contribute and use the funds for medical expenses.

- For your FSA, you generally have a few options: you can roll it over to an HSA if you’re eligible, spend it within a grace period or limited carryover amount, or transfer it to a new employer if they offer a similar plan.

Are there any tax benefits to using an HSA or FSA?

Yes, both HSAs and FSAs provide significant tax benefits:

- Tax-deductible contributions: Contributions are made with pre-tax dollars, lowering your taxable income.

- Tax-free growth: For HSAs, funds grow tax-free. For FSAs, contributions are also made on a pre-tax basis.

- Tax-free withdrawals: For HSAs, withdrawals for qualified medical expenses are tax-free. FSAs are also tax-free for withdrawals used for qualified medical expenses.