Plunging into the complexities of healthcare finance, a compelling option emerges—the Anthem Health Savings Account (HSA). As healthcare costs surge, understanding this financial tool becomes critical for both individuals and families aiming for fiscal prudence. This article dissects the HSA’s intricacies, delivering expert insights, evidence-based statements, and real-world examples, all while integrating natural keywords seamlessly.

Unveiling the Anthem Health Savings Account

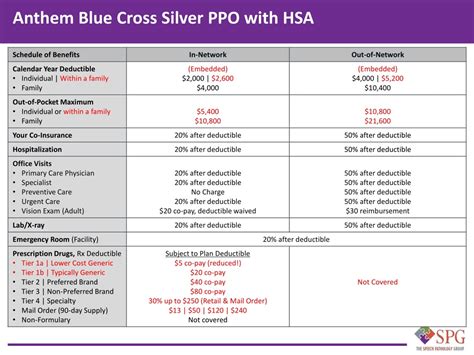

The Anthem Health Savings Account serves as a trifecta blend of tax benefits, medical flexibility, and a mechanism for long-term savings. This specialized account allows eligible individuals to deposit pre-tax income into a savings account, to be utilized for qualified medical expenses tax-free. When paired with a high-deductible health plan (HDHP), the HSA provides an avenue for managing out-of-pocket costs efficiently while fostering personal fiscal responsibility.Key Insights

- Primary insight with practical relevance: HSAs can lead to substantial savings through tax advantages and can cover medical expenses that insurance does not.

- Technical consideration with clear application: Contributions roll over annually and can be invested for growth, providing long-term financial benefits.

- Actionable recommendation: Individuals should maximize their HSA contributions, especially if they have a high-deductible health plan, to leverage both immediate tax savings and future medical expenses coverage.

Maximizing the Benefits of the Anthem HSA

One of the standout features of the Anthem Health Savings Account is its tax advantages. Contributions are made with pre-tax dollars, reducing taxable income while simultaneously building a reserve for medical expenses. Moreover, withdrawals for qualified medical expenses are tax-free, a significant benefit in an era where healthcare costs are skyrocketing. For instance, consider a family with a modest high-deductible plan—an HSA provides them with the means to manage and reduce out-of-pocket costs like co-pays, deductibles, and even some non-prescription medications.Investment Opportunities within the Anthem HSA

Beyond the immediate tax benefits, an HSA offers a unique opportunity for investment. Unlike traditional savings accounts, the funds within an HSA can be invested in a variety of vehicles, such as stocks, bonds, and mutual funds, provided the account holder is at least 65 years old or meets other criteria allowing for IRA-like investment options. This provision is particularly beneficial for those looking to grow their medical expense reserves over time. For example, an individual contributing the maximum allowable limit each year, investing wisely, could accumulate a substantial sum that covers major medical procedures or health-related expenses in retirement, effectively turning the HSA into a healthcare pension.Is everyone eligible to open an Anthem HSA?

Not everyone qualifies for an HSA. To open an Anthem Health Savings Account, an individual must be enrolled in a high-deductible health plan (HDHP) and cannot be eligible for Medicare or have other health coverage except for certain allowed exceptions such as dental, vision, and long-term care insurance.

What happens to the money in an HSA if I switch health plans?

The funds in your HSA roll over from year to year, regardless of changes in health insurance coverage. You retain ownership of the account and all contributions and earnings, regardless of life changes like switching jobs or health plans. This ensures your healthcare savings are always there when needed.

In conclusion, the Anthem Health Savings Account stands as an exemplary financial instrument for those navigating the labyrinth of healthcare expenses. With its blend of tax advantages, investment potential, and the flexibility to cover an array of medical costs, the HSA offers a well-rounded approach to healthcare finance. Embracing this tool can lead to significant savings, both in the present and for future healthcare needs.