Understanding 2025 United Health Plans: A Comprehensive Guide

Are you overwhelmed with choosing the right health plan for 2025? With an array of options, it’s easy to feel lost. This guide will walk you through the essentials of United Health Plans for 2025, offering clear and practical advice to help you make an informed decision that best meets your healthcare needs. Whether you’re a newcomer or someone looking to switch plans, this guide will provide actionable steps and real-world examples to simplify your understanding.

Why This Guide Matters

Navigating health insurance can be daunting, especially when faced with a multitude of plans that seem complex and obscure. Our goal is to demystify the process and provide you with straightforward, actionable advice. This guide focuses on your needs, presenting a clear roadmap to the most suitable United Health Plan for 2025. By addressing your pain points directly, we aim to empower you to make confident, informed choices for your health coverage.

Quick Reference

Quick Reference

- Immediate action item with clear benefit: Check your current benefits and eligibility for any changes in 2025 plans.

- Essential tip with step-by-step guidance: Start with a clear list of what you need in a health plan (e.g., preferred doctors, prescription coverage).

- Common mistake to avoid with solution: Assuming one plan fits all; always read the fine print and compare multiple options.

Understanding Key Components of 2025 United Health Plans

To make an informed decision, it’s crucial to understand the core components of 2025 United Health Plans. Here we break down the essentials you need to know to choose the right plan.

Coverage Levels and Plan Types

United Health Plans in 2025 offer a range of coverage levels including HMOs, PPOs, EPO, and POS plans. Each has its unique benefits and network restrictions.

- HMO (Health Maintenance Organization): Often requires you to choose a primary care physician and get referrals for specialists. It generally has lower out-of-pocket costs.

- PPo (Preferred Provider Organization): Offers more flexibility to see specialists without referrals. It usually has higher premiums and deductibles.

- EPO (Exclusive Provider Organization): Allows you to only receive care from a network of providers, but no referrals are needed. It generally has higher out-of-pocket costs compared to HMOs.

- POS (Point of Service): Combines elements of HMOs and PPOs. Requires a primary care physician but allows visits to out-of-network providers without a referral for an additional cost.

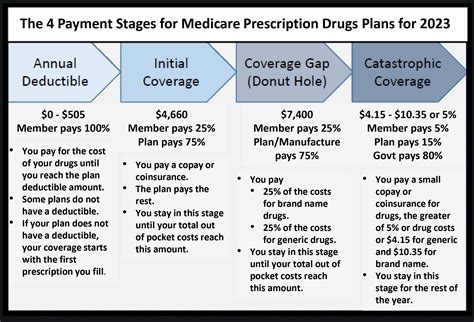

Cost-Sharing Components

Understanding how costs are shared between you and your health plan is crucial. Here are the main cost-sharing elements:

- Premiums: The monthly fee for your health plan.

- Deductibles: The amount you pay out-of-pocket before your insurance starts to pay for covered services.

- Copayments and Coinsurance: The amounts you pay for services after you meet your deductible.

- Out-of-Pocket Maximum: The maximum amount you pay in a year for covered services.

How to Choose the Right Plan for You

Making the right choice for your health plan involves understanding your personal healthcare needs, evaluating different options, and comparing cost-sharing components. Here’s a detailed guide to help you through the process.

Step 1: Assess Your Healthcare Needs

Start by thinking about your personal healthcare needs. Consider the following:

- Frequency of doctor visits

- Need for specialists or emergency care

- Current prescription medications

- Existing health conditions

Use this assessment to prioritize the type of plan that fits your needs. For instance, if you frequently visit specialists, a PPO might be more suitable than an HMO.

Step 2: Evaluate Plan Networks

Different plans have different networks of doctors and hospitals. Review the provider networks for each plan:

- Check if your current doctors and hospitals are in the plan’s network.

- Review the network size and its geographic coverage.

- Note any specialized services available through the network (e.g., orthopedics, mental health).

Step 4: Compare Costs

Carefully compare the cost structures of each plan:

- Premiums: Look at the monthly premium costs and decide what you can afford.

- Deductibles: Understand the out-of-pocket amount you will need to pay before insurance coverage kicks in.

- Copayments and Coinsurance: Compare the percentages and fixed amounts you will pay for services.

- Out-of-Pocket Maximum: This is the maximum amount you will pay in a year, after which your plan covers 100% of the costs.

For example, if you have high medical expenses, a plan with a lower premium and higher deductible might be beneficial, as it ensures lower monthly costs, albeit higher initial expenses.

Step 5: Review Additional Benefits and Services

Some plans offer additional benefits not covered in the basic structure:

- Preventive services: Check if the plan covers preventive services like vaccines, screenings, and annual check-ups at no extra cost.

- Wellness programs: Some plans offer wellness programs that may include gym memberships or smoking cessation programs.

- Telehealth services: Increasingly popular, consider plans that offer telehealth options.

Practical FAQ

What should I do if I miss the enrollment period?

Missing the standard enrollment period can be challenging, but you may still have options: Special Enrollment: You may qualify for a special enrollment period if you experience a qualifying life event such as marriage, birth of a child, or loss of other health coverage. Solution: Contact United Health customer service to inquire about your specific situation and potential for special enrollment. Be prepared to provide documentation for your qualifying event.

How can I find out if my medications are covered?

To check if your medications are covered: Step 1: Log into your United Health plan portal or use their mobile app. Step 2: Navigate to the pharmacy benefits section. Step 3: Use the formulary tool to search for your medications. Best Practice: Always keep a list of your medications and check coverage before starting any new prescriptions.

What is a Health Savings Account (HSA) and how does it work with my United Health Plan?

A Health Savings Account (HSA) is a tax-advantaged account that can be used to pay for qualified medical expenses with pre-tax dollars. How it works:

- Contributions: You can contribute pre-tax dollars to your HSA, which are not subject to federal income tax.

- Earnings: The money in your HSA can grow tax-free over time.

- Usage: Withdrawals for qualified medical expenses are tax-free; withdrawals for non-qualified expenses are taxable and subject to a 20% penalty.